Physical Address

Austin, TX, USA

Physical Address

Austin, TX, USA

Being your own boss has incredible perks—freedom, flexibility, and full control of your work. But when it comes to health insurance, being self-employed in the USA can get tricky. Without an employer to sponsor a plan, freelancers, gig workers, and entrepreneurs must find coverage on their own.

The good news? You have plenty of options—and with smart planning, you can get affordable, comprehensive coverage that fits your lifestyle and budget.

💬 Quote to Remember:

“Health insurance isn’t just an expense—it’s your financial safety net against life’s unexpected turns.”

In this detailed guide, we’ll explore the best health insurance plans for self-employed Americans, compare top providers, and break down how to choose the right one based on your needs and location.

The Affordable Care Act (ACA) Marketplace is the best starting point for most self-employed individuals. These plans cover essential health benefits such as:

You can apply for subsidies based on your income, which can significantly lower monthly premiums.

Tip: If your income fluctuates as a freelancer, estimate conservatively to avoid owing money at tax time.

If your income falls below a certain threshold, Medicaid offers comprehensive coverage at little or no cost. Eligibility and benefits vary by state, but most include hospital care, doctor visits, and prescriptions.

Many self-employed people mistakenly assume they won’t qualify, but even part-time freelancers can apply if their household income is low.

Example: In many states, a single adult earning under $20,000 annually may qualify for full Medicaid coverage.

If you prefer more flexibility or missed the ACA enrollment window, you can buy private health insurance directly from insurers. These plans:

However, they’re generally more expensive and don’t qualify for federal subsidies. Always compare premiums, deductibles, and coverage details before committing.

Organizations like the National Association for the Self-Employed (NASE) and the Freelancers Union provide access to group health insurance.

Benefits include:

If you’re married or under 26, one of the simplest options is joining a spouse’s or parent’s employer-sponsored health plan.

These group plans often come with:

This option is particularly helpful if you’re just starting out or transitioning into full-time self-employment.

If you’ve recently left a job, you might qualify for COBRA—a law allowing you to continue your employer’s health insurance for up to 18 months.

Pros: You keep your current coverage.

Cons: You must pay the full premium plus a 2% admin fee, which can be pricey.

COBRA is best as a temporary solution while you explore longer-term coverage options.

These community-based programs (like Medi-Share or Liberty HealthShare) aren’t traditional insurance. Instead, members pool funds to cover each other’s medical bills.

Pros:

Cons:

These are best for those with minimal healthcare needs and strong financial discipline.

Short-term plans are ideal if you’re between jobs or waiting for ACA coverage. They can last from one month up to a year.

While affordable, they come with major limitations:

Use them only as a temporary safety net, not a long-term solution.

Finding the right provider is just as important as choosing the plan type. Here are some of the top-rated options based on coverage, cost, and availability:

Downside: Only available in 8 states and D.C., and no PPO options on the Marketplace.

Perfect choice if Kaiser isn’t available in your area.

If you choose a High-Deductible Health Plan (HDHP), you can open an HSA to save tax-free money for medical expenses.

HSAs not only reduce taxable income but also serve as long-term health savings vehicles.

Self-employed individuals can deduct 100% of their health insurance premiums on their federal tax return, even if they don’t itemize deductions.

This includes coverage for yourself, your spouse, and dependents.

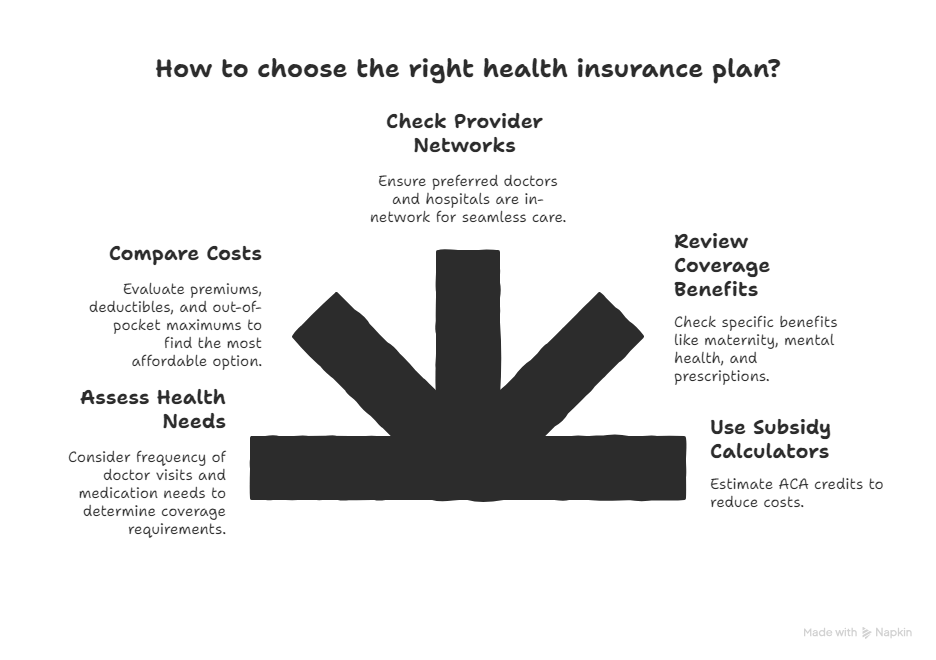

Choosing the best plan isn’t just about price—it’s about matching coverage with your lifestyle. Follow these steps:

| State | Top Provider (2025) | Highlight |

|---|---|---|

| Florida | Florida Blue (BCBS) | Strong statewide network |

| Texas | Ambetter Health | Affordable ACA plans |

| New York | Fidelis Care | Great for freelancers |

| New Jersey | Horizon BCBS | Broad plan options |

| Michigan | Priority Health | Excellent HSA-compatible plans |

| Washington | Premera Blue Cross | High-rated customer service |

| North Carolina | BCBS NC | Affordable PPO options |

| Illinois | Molina Healthcare | Low-cost ACA plans |

| Georgia | Ambetter | Best for budget coverage |

| Virginia | Anthem BCBS | Top-rated family plans |

| Oregon | Moda Health | Great HSA plans |

| Colorado | Kaiser Permanente | Excellent integrated care |

✅ Review your income annually to adjust subsidy eligibility.

✅ Keep records of all premium payments for tax deductions.

✅ Consider combining an HSA with an HDHP for long-term savings.

✅ Compare insurers yearly—plans and premiums can change.

For self-employed Americans, health insurance isn’t optional—it’s essential. From ACA Marketplace plans to private and group options, there’s a policy for every income and lifestyle.

By comparing top providers, leveraging tax deductions, and planning ahead, you can protect both your health and your business.