Physical Address

Austin, TX, USA

Physical Address

Austin, TX, USA

A credit score is more than just a number — it’s a key that can open (or close) financial doors in your life. Whether you’re applying for a credit card, home loan, or even renting an apartment, your credit score speaks volumes about your financial reliability.

In this guide, we’ll explain what a credit score is, how it’s calculated, what score is considered “good,” and why it matters so much — especially if you live in the USA in 2025. By the end, you’ll understand exactly how credit scoring works and how you can improve yours to secure better opportunities.

A credit score is a three-digit number that represents your creditworthiness — or how likely you are to repay borrowed money responsibly. The score typically ranges from 300 to 850, where higher numbers indicate stronger credit history and lower risk for lenders.

Most lenders in the U.S. rely on two main scoring systems:

These systems use data from the three major credit bureaus — Experian, Equifax, and TransUnion — to generate your score based on your financial behavior.

| Credit Score Range | Rating | Meaning |

|---|---|---|

| 800–850 | Excellent | Exceptional credit management, top loan offers |

| 740–799 | Very Good | Above average; qualifies for low-interest rates |

| 670–739 | Good | Average borrower; generally accepted by most lenders |

| 580–669 | Fair | Some lenders may approve with higher interest rates |

| 300–579 | Poor | High risk; most applications likely to be denied |

👉 A credit score above 700 is considered good in the USA, while anything above 800 is excellent.

Credit scores aren’t just used by banks. Many organizations check them to assess your reliability:

In short, your credit score affects almost every major financial decision in your life.

Understanding how credit scores are calculated is essential for managing them wisely. The FICO Score model, used by about 90% of U.S. lenders, is based on five weighted factors:

This is the most important factor. It tracks whether you’ve paid your bills on time.

This measures your credit utilization ratio — how much of your available credit you’re using.

Example: If your credit card limit is $10,000 and you owe $3,000, your utilization is 30%.

✅ Tip: Try to keep utilization below 30%, and ideally under 10% for top scores.

Lenders like to see a long history of responsible credit use. This includes the age of your oldest and newest accounts, plus the average account age.

✅ Tip: Don’t close old credit cards unless necessary — they help maintain credit history.

A mix of credit types (credit cards, car loans, mortgages, student loans, etc.) shows lenders that you can manage various kinds of debt responsibly.

✅ Tip: Having both revolving (credit card) and installment (loan) credit types can improve your score.

Opening multiple new accounts in a short period can signal risk to lenders. Each application triggers a hard inquiry, which can lower your score slightly.

✅ Tip: Avoid applying for several new credit lines within a few months.

Both FICO and VantageScore aim to predict credit risk, but they differ slightly in methodology.

| Feature | FICO Score | VantageScore |

|---|---|---|

| Scale | 300–850 | 300–850 |

| Most Influential Factor | Payment History | Total Credit Usage |

| Time Required to Generate Score | 6 months of credit history | 1 month of activity |

| Used By | 90% of U.S. lenders | Increasingly common for free credit reports |

Is FICO score the same as a credit score?

Not exactly — FICO is a type of credit score, but not the only one. Think of “credit score” as the category and “FICO” as a specific brand.

In 2025, according to Experian and FICO data:

| Credit Bureau | Good Credit Range | Excellent Credit Range |

|---|---|---|

| Experian | 670–739 | 740–850 |

| Equifax | 670–749 | 750–850 |

| TransUnion | 660–724 | 725–850 |

| Credit Karma (Estimate) | 700+ | 780+ |

These ranges may differ slightly, but they all indicate how lenders view your financial reliability.

Credit scores usually update every 30–45 days, depending on how often your creditors report new data to the credit bureaus.

Major credit bureaus update scores when:

If you’re actively improving your credit, you might start seeing positive results within 1–3 months.

Your credit score influences more than loan approvals — it affects how much you pay for things like interest, rent, and even insurance.

Here’s how a high credit score can save you money:

Conversely, a poor score can cost thousands in extra interest over a lifetime.

💬 Example:

A borrower with a 760 credit score might get a 5% mortgage rate, while someone with a 620 score could face 7%. On a $300,000 home loan, that’s over $100,000 more in interest across 30 years!

Here are some common habits that can drag your score down:

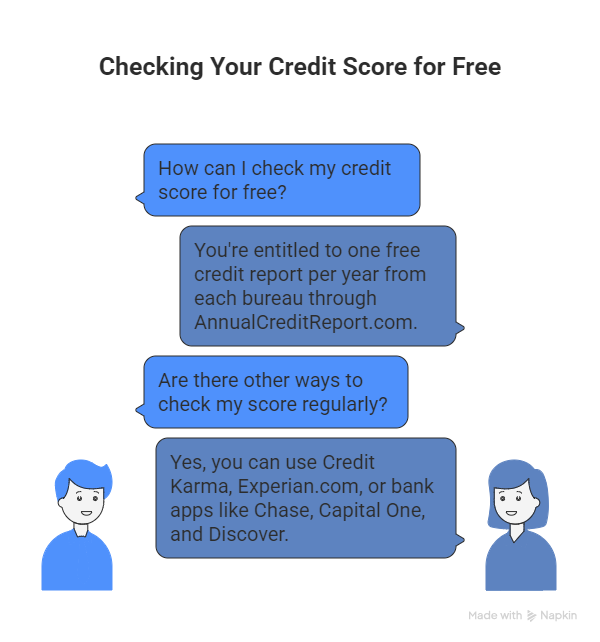

You’re entitled to one free credit report per year from each bureau through AnnualCreditReport.com — the official government-authorized source.

You can also check your scores regularly via:

Checking your credit this way counts as a soft inquiry — it won’t hurt your score.

As of early 2025:

States with the highest averages include Minnesota (742) and Vermont (738), while Mississippi and Louisiana have the lowest, averaging around 680.

The FICO Score 8 remains the most widely used version. It’s known for:

Newer models like FICO 9 and FICO 10T add rental payments and trended data, offering a more detailed look at financial patterns.

A great credit score is built over time with consistency, discipline, and awareness. Whether you’re just starting out or rebuilding after financial setbacks, following these habits can help:

With patience and consistency, your score can climb from “fair” to “excellent” — unlocking better financial freedom.

| Credit Factor | Weight | Action Tip |

|---|---|---|

| Payment History | 35% | Always pay on time |

| Amounts Owed | 30% | Keep utilization under 30% |

| Credit History Length | 15% | Keep old accounts active |

| Credit Mix | 10% | Use both credit cards & loans |

| New Credit | 10% | Space out applications |