Physical Address

Austin, TX, USA

Physical Address

Austin, TX, USA

Health insurance can feel complicated filled with confusing terms, endless plan options, and fine print that seems written in another language. But understanding the basics of health insurance in the USA can save you money, reduce stress, and help you make smarter health decisions.

Think of it like this: health insurance isn’t just a card in your wallet it’s financial protection for your body. Whether you’re visiting a doctor for a routine check-up, dealing with an unexpected injury, or managing a chronic condition, having the right health insurance plan ensures you get care without breaking the bank.

📜 Quote about health insurance:

“Health insurance doesn’t just protect your wallet, it protects your peace of mind.”

In 2026, with medical costs continuing to rise, not having insurance can mean paying thousands of dollars out-of-pocket for even basic treatments. That’s why understanding health insurance basics USA is more important than ever. Once you grasp how plans work, what terms like “deductible” or “copay” mean, and how to choose coverage that fits your lifestyle, you’ll be able to confidently make decisions that protect both your health and your finances.

At its core, health insurance is a contract between you and an insurance company. You agree to pay a regular fee (called a premium), and in exchange, the insurance company agrees to help pay for your medical expenses when you get care.

These expenses can include:

The goal is simple — to protect you from unexpected, high medical costs. Without health insurance, a single emergency room visit or operation could drain your savings.

Here’s how it works in practice:

For example:

If your plan has a $2,000 deductible, 20% coinsurance, and an $8,000 out-of-pocket maximum, you’ll pay the first $2,000 for covered services. After that, your insurer pays 80%, and you pay 20%, until you hit $8,000.

🩺 Why it matters:

Health insurance gives you access to preventive care — like annual checkups, vaccinations, and screenings — that can detect problems early and save lives. It also ensures that you aren’t financially devastated by medical emergencies.

💬 Health insurance

“The best time to understand health insurance is before you need it.”

From individual coverage and employer plans to marketplace health insurance in Florida or Virginia health insurance exchange options, every plan follows the same basic principle — pay a little now to avoid paying a lot later.

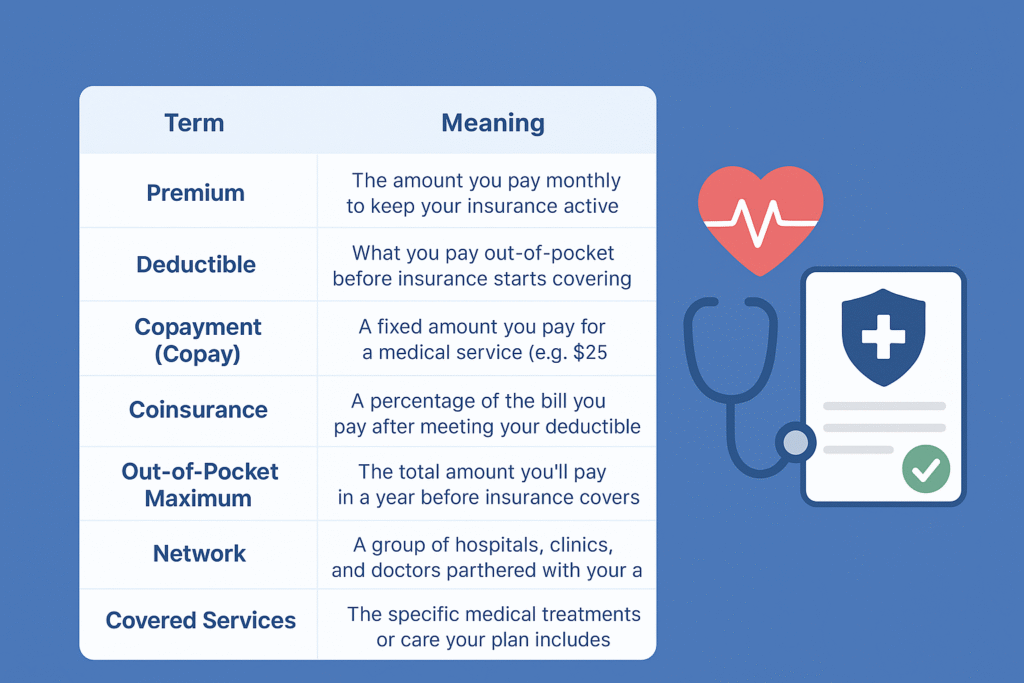

Before you dive into buying a plan or comparing quotes about health insurance, it’s important to understand the core terms you’ll see again and again. These terms form the foundation of how health insurance in the USA works — and knowing them can save you from expensive surprises later.

💡 Pro Tip: Before scheduling a visit, always confirm if your doctor or hospital is in-network. Going out-of-network can lead to much higher bills that your health insurance may not cover.

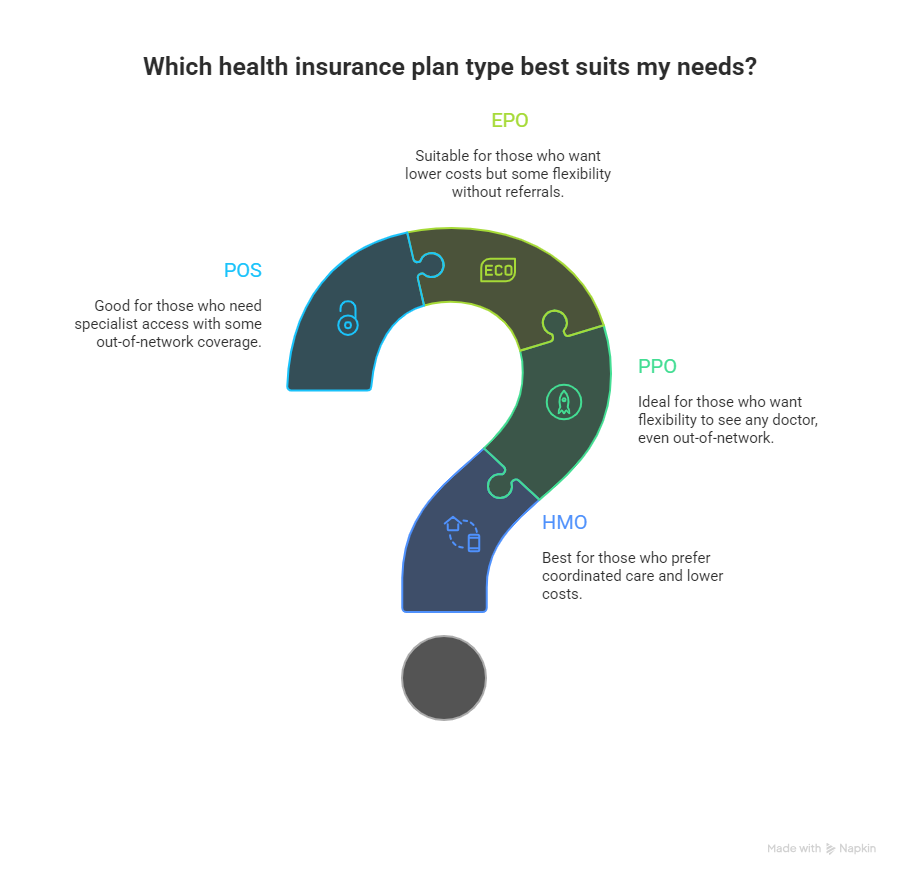

Choosing the right type of health insurance plan can feel overwhelming — especially with so many options out there. But once you understand how each plan works, you can match one to your lifestyle, budget, and healthcare needs.

Here’s a breakdown of the main types of health insurance in the USA:

| Plan Type | Description | Best For |

|---|---|---|

| HMO (Health Maintenance Organization) | HMO plans require you to use in-network doctors and get referrals from your primary care provider before seeing a specialist. They tend to have lower monthly premiums and out-of-pocket costs but less flexibility. | Best for those who want affordable, coordinated care through one doctor managing most of their treatment. |

| PPO (Preferred Provider Organization) | PPO plans offer more freedom — you can visit any doctor, even outside your network, without referrals. However, this flexibility comes at a higher cost. | Great for people who travel often or prefer choosing their own doctors without needing permission. |

| EPO (Exclusive Provider Organization) | With an EPO plan, you don’t need referrals for specialists, but coverage is limited to in-network providers (except in emergencies). These plans are cost-effective for those who stay within their network. | Ideal for individuals who want lower costs but still prefer flexibility without referrals. |

| POS (Point of Service) | POS plans blend features of HMO and PPO. You’ll need referrals for specialists but can go out-of-network if you’re willing to pay more. | Perfect for people who value coordinated care but still want the option of going out-of-network occasionally. |

🩺 Example:

If you’re in Virginia, you might explore the Virginia Health Insurance Exchange, which lists both private and government-backed plans (like through Healthcare.gov). Similarly, states like Ohio, Arizona, and Florida offer marketplace health insurance options for residents through their exchanges.

💼 For Small Businesses:

Many small businesses struggle to find affordable coverage for their employees. Thankfully, there are now specific programs and health insurance innovations that make offering group coverage easier and more affordable. Platforms like the Virginia Health Insurance Exchange or Marketplace Health Insurance in Florida are great starting points.

Understanding how health insurance costs are structured is key to managing your medical expenses wisely. Your total cost isn’t just one number — it’s made up of multiple components that work together to define how much you’ll pay throughout the year.

Let’s break it down 👇

Your premium is the amount you pay every month to keep your health insurance active — even if you don’t visit a doctor.

Think of it like a subscription that guarantees your medical coverage is always ready when needed.

The deductible on health insurance is the amount you pay out of pocket before your plan begins to share the costs.

Example:

If your deductible is $1,500, you’ll pay for the first $1,500 in medical services yourself. After that, your insurer starts paying their share.

This is one of the most important terms to understand when learning health insurance basics in the USA.

Once your deductible is met, you’ll still pay a copay or coinsurance for services.

These small payments add up over time, so always include them in your budget planning.

This is your financial safety net — the maximum amount you’ll pay in a year for covered services. Once you reach this limit, your insurer covers 100% of all additional covered costs.

Most insurance providers have a network of doctors, hospitals, and clinics that offer discounted rates.

Going in-network keeps your costs lower, while out-of-network care can be much more expensive — or sometimes not covered at all.

🧠 Smart Tip:

If you’re generally healthy and rarely visit the doctor, a high-deductible health plan (HDHP) might make sense because it has lower monthly premiums. But if you expect regular care or have ongoing health needs, a low-deductible plan can save you more in the long run.

The U.S. government offers several federal health insurance programs to make healthcare accessible and affordable for everyone. Whether you’re a senior, a parent, or self-employed, there’s likely a program designed to fit your situation.

Medicare provides health insurance for Americans aged 65+ or for individuals with certain disabilities.

It’s divided into several parts:

Medicare helps millions manage healthcare costs after retirement, acting as a cornerstone of senior health coverage.

Medicaid is a joint federal-state program that offers free or low-cost health insurance to low-income individuals and families.

Each state manages its own eligibility and coverage details — so benefits in Virginia may differ from those in Arizona or Ohio.

If you live in Virginia, you can apply through the Virginia Health Insurance Exchange or the state’s Medicaid website.

CHIP provides affordable health insurance for children in families that earn too much to qualify for Medicaid but can’t afford private insurance.

It covers doctor visits, dental care, immunizations, and more — ensuring kids receive consistent, quality care.

Enacted in 2010, the Affordable Care Act (also known as Obamacare) revolutionized health insurance in the USA.

Here’s how it helps:

You can explore and enroll in Marketplace Health Insurance plans at HealthCare.gov, or through your state’s exchange — such as the Virginia Health Insurance Exchange or Marketplace Health Insurance in Florida.

Choosing the right health insurance plan isn’t just about finding the cheapest option — it’s about finding one that actually meets your medical and financial needs. With hundreds of options across states like Florida, Ohio, Virginia, and Arizona, it’s easy to get overwhelmed. Here’s a step-by-step way to make a confident choice 👇

Start by reviewing your past year’s healthcare usage.

Do you visit the doctor often? Need regular prescriptions or therapy sessions?

If you have chronic conditions or a growing family, pick a plan with a low deductible and strong coverage.

If you’re healthy and rarely visit a clinic, a high-deductible plan can save you money on monthly premiums.

💬 Quote about health insurance:

“Health insurance is not an expense — it’s an investment in your peace of mind and protection.”

Every insurer has a network of preferred doctors, clinics, and hospitals.

Make sure your trusted healthcare providers are in-network to avoid surprise bills.

You can usually verify this on the insurer’s website or through the Health Insurance Marketplace.

Each plan comes with a mix of premiums, deductibles, copays, and coinsurance.

Understanding what are deductibles in health insurance is key: it’s the amount you pay before your insurer starts contributing.

For low monthly premiums, you’ll often face higher out-of-pocket costs — and vice versa.

🧠 Pro Insight:

For many small businesses and health insurance buyers, balancing these two factors (premium vs. deductible) is the secret to affordable coverage that still delivers value.

Not all medications are covered under every plan. Review the formulary — the list of covered drugs — to make sure your prescriptions are included.

If not, you could face hundreds in extra monthly costs.

Modern plans offer more than just hospital coverage.

Look for extras like:

These benefits can add huge long-term value, especially for families or remote workers.

✨ Pro Tip:

If you’re young, single, or self-employed, a high-deductible health plan (HDHP) paired with a Health Savings Account (HSA) can be smart.

It offers lower premiums, tax advantages, and flexible savings for future medical expenses.

But for families, seniors, or those with regular medical visits — a low-deductible plan provides more stability and predictable costs.

Navigating health insurance in the USA may seem complex at first, but once you grasp the basics — premiums, deductibles, copays, and networks — everything starts to make sense.

Health insurance isn’t just paperwork or numbers; it’s financial security that protects you when life takes an unexpected turn. Whether you’re buying coverage through the Virginia Health Insurance Exchange, exploring Marketplace health insurance in Florida, or reviewing private options in Ohio or Arizona, the goal remains the same — protect your health and your future.

🧠 Final Takeaway

Health insurance is your safety net — ensuring one medical emergency doesn’t become a financial disaster.

With the right knowledge and plan, you can confidently safeguard your well-being while saving money.

And that’s what understanding health insurance basics in the USA is all about — peace of mind, protection, and smarter choices for 2026 and beyond. 🩺🇺🇸